Making the Most of Credit Cards for Your Field Teams

Making the Most of Credit Cards for Your Field Teams

You want your field teams to move quickly. You don’t want jobs slowed down because your team is waiting on purchase orders or relying on office approvals for urgent purchases.

At the same time, you want confidence that company credit cards are being used for the job, not personal rewards or convenience spending.

The solution is a modern card program with automated guardrails so company cards are used appropriately.

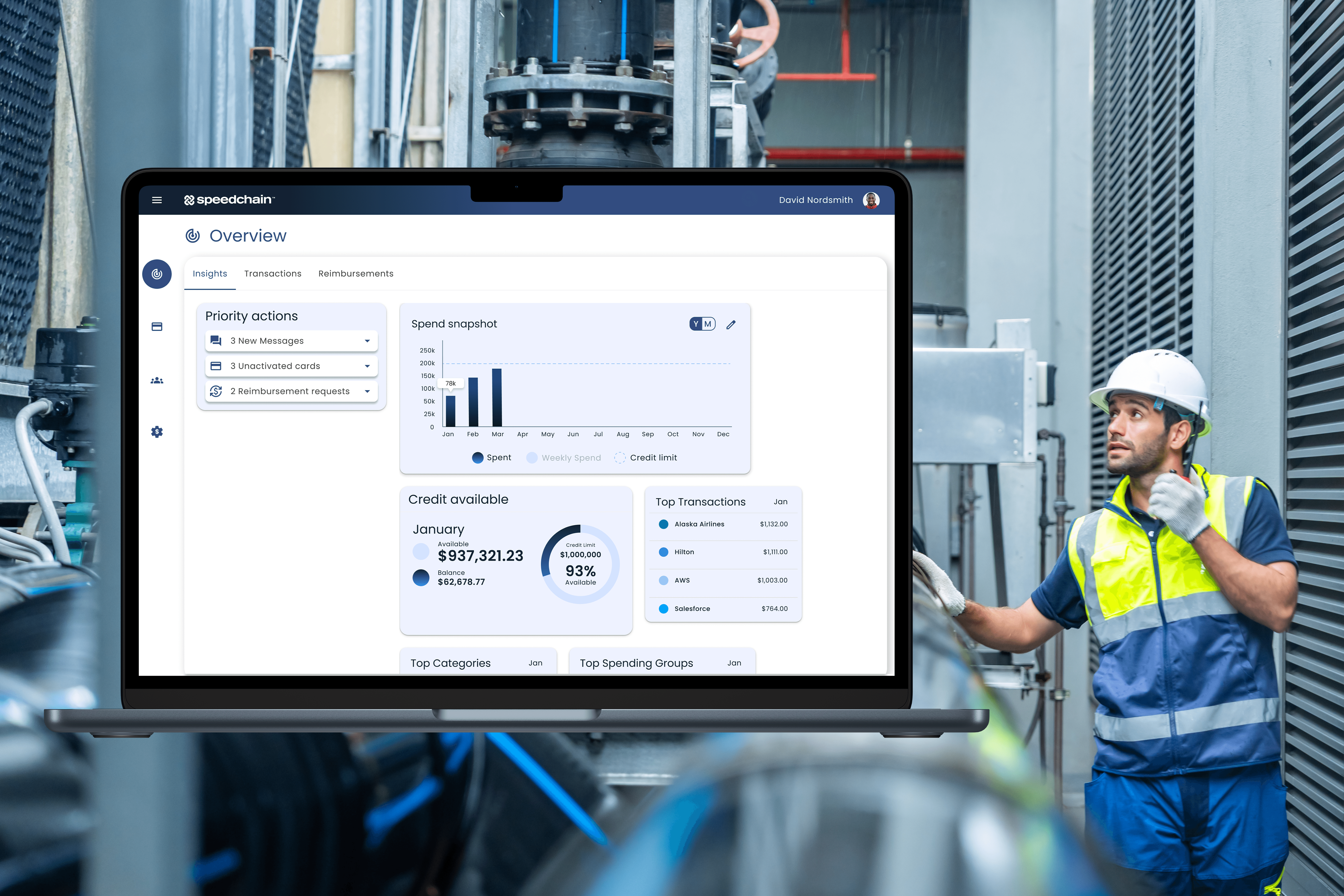

Modern credit card programs give you transaction limits, spend rules, receipt capture, and routed approvals, while automatically blocking questionable transactions.

Strong modern card programs mean you do not need to rely on trust alone. They are designed so the right spending behavior is easy and the wrong behavior is uncomfortable.

Start with who needs what freedom

The first step to implementing a modern card program is designating access by role.

Group cardholders into simple categories:

Foremen and superintendents who handle daily runs for materials, fuel, and small tools.

Project engineers and coordinators who manage occasional vendor payments, permits, and deposits.

Project leaders who handle travel and client-facing spend.

Office staff who purchase software, office supplies, and overhead items.

For each group, decide three things:

How much they typically need to spend in a given week.

What types of purchases are in scope for their role.

Who should review their transactions before they post.

Once you define these guidelines, credit card spend limits start to make sense. A superintendent may need room for materials and urgent jobsite purchases but not for large travel expenses. An executive may need broader flexibility but still benefit from reasonable per-transaction caps.

Legitimate business purchases go through smoothly, and large questionable ones stand out clearly when card limits reflect your team’s different work patterns.

Use spend rules to prevent mistakes

Dollar limits are a good baseline, but they are not strong enough on their own. Spend rules are the next layer in deciding where a card can be used in the first place.

Most field cards should allow categories like building materials, fuel, equipment rental, and hotels for job-related travel.

At the same time, they can block categories that have little connection to job execution, such as convenience stores, luxury retail, or broad online marketplaces where it is impossible to tell whether a charge is job-related or personal.

Spend rules prevent card misuse and send a clear signal to the field about what the card is intended for. Individual judgment still matters, but your system now reinforces expectations before a transaction is made.

Make receipts and coding easy for all teams

Card control depends on visibility, and visibility depends on how easily information is captured at the right time.

The best time to collect receipts and job details is immediately after a purchase, while the superintendent is still at the supply house or sitting in their truck.

For field teams, that means a mobile app where they can snap a receipt photo and select a job or cost code right after they make a purchase. For finance, it means a clear view of which transactions are missing information without needing to skim credit card statements.

Some teams choose to reinforce receipts and coding by tying card access to program compliance. A cardholder may have a short window, for example three days from the transaction date, to submit receipts before their card is temporarily locked. The card platform handles automatic reminders and lock out enforcement, giving time back to your accounts payable team.

Route approvals where the work happens

Spend approvals work smoothly when they reflect the structure of how your projects are managed.

The most effective first reviewers for field spend are usually project managers, senior superintendents, or regional leaders who understand the job context and can quickly spot charges that do not belong.

Finance remains the final gate before transactions post to the ERP, but the first review happens close to the work.

Approvals can follow the organizational chart or the job structure. What matters is that transactions, receipts, and approvals live in one system with a clear record of who approved what and when, so the audit trail is always available.

Bringing it together

When role-based limits, spend rules, receipt capture, and project-level approvals work in tandem, field teams gain speed with better guardrails.

Signs your card program is streamlined:

Routine purchases flow through without friction.

Exceptions surface quickly and go to the right reviewer.

Finance sees spend when it happens, giving time to course correct.

Final thoughts

Limiting the number of cardholders on your team or layering on manual approvals often slows the build and increases workarounds.

A more streamlined approach is implementing a modern card program with workflows that incentivize team compliance without adding friction.

As you review your current card program, ask where routine purchases feel harder than they should be, where field spend is most difficult to see in your reporting, and which card approvals depend on emails and spreadsheets.

These answers help you determine where a modern card program with streamlined controls can make spend management automated, efficient, and easy.

You want your field teams to move quickly. You don’t want jobs slowed down because your team is waiting on purchase orders or relying on office approvals for urgent purchases.

At the same time, you want confidence that company credit cards are being used for the job, not personal rewards or convenience spending.

The solution is a modern card program with automated guardrails so company cards are used appropriately.

Modern credit card programs give you transaction limits, spend rules, receipt capture, and routed approvals, while automatically blocking questionable transactions.

Strong modern card programs mean you do not need to rely on trust alone. They are designed so the right spending behavior is easy and the wrong behavior is uncomfortable.

Start with who needs what freedom

The first step to implementing a modern card program is designating access by role.

Group cardholders into simple categories:

Foremen and superintendents who handle daily runs for materials, fuel, and small tools.

Project engineers and coordinators who manage occasional vendor payments, permits, and deposits.

Project leaders who handle travel and client-facing spend.

Office staff who purchase software, office supplies, and overhead items.

For each group, decide three things:

How much they typically need to spend in a given week.

What types of purchases are in scope for their role.

Who should review their transactions before they post.

Once you define these guidelines, credit card spend limits start to make sense. A superintendent may need room for materials and urgent jobsite purchases but not for large travel expenses. An executive may need broader flexibility but still benefit from reasonable per-transaction caps.

Legitimate business purchases go through smoothly, and large questionable ones stand out clearly when card limits reflect your team’s different work patterns.

Use spend rules to prevent mistakes

Dollar limits are a good baseline, but they are not strong enough on their own. Spend rules are the next layer in deciding where a card can be used in the first place.

Most field cards should allow categories like building materials, fuel, equipment rental, and hotels for job-related travel.

At the same time, they can block categories that have little connection to job execution, such as convenience stores, luxury retail, or broad online marketplaces where it is impossible to tell whether a charge is job-related or personal.

Spend rules prevent card misuse and send a clear signal to the field about what the card is intended for. Individual judgment still matters, but your system now reinforces expectations before a transaction is made.

Make receipts and coding easy for all teams

Card control depends on visibility, and visibility depends on how easily information is captured at the right time.

The best time to collect receipts and job details is immediately after a purchase, while the superintendent is still at the supply house or sitting in their truck.

For field teams, that means a mobile app where they can snap a receipt photo and select a job or cost code right after they make a purchase. For finance, it means a clear view of which transactions are missing information without needing to skim credit card statements.

Some teams choose to reinforce receipts and coding by tying card access to program compliance. A cardholder may have a short window, for example three days from the transaction date, to submit receipts before their card is temporarily locked. The card platform handles automatic reminders and lock out enforcement, giving time back to your accounts payable team.

Route approvals where the work happens

Spend approvals work smoothly when they reflect the structure of how your projects are managed.

The most effective first reviewers for field spend are usually project managers, senior superintendents, or regional leaders who understand the job context and can quickly spot charges that do not belong.

Finance remains the final gate before transactions post to the ERP, but the first review happens close to the work.

Approvals can follow the organizational chart or the job structure. What matters is that transactions, receipts, and approvals live in one system with a clear record of who approved what and when, so the audit trail is always available.

Bringing it together

When role-based limits, spend rules, receipt capture, and project-level approvals work in tandem, field teams gain speed with better guardrails.

Signs your card program is streamlined:

Routine purchases flow through without friction.

Exceptions surface quickly and go to the right reviewer.

Finance sees spend when it happens, giving time to course correct.

Final thoughts

Limiting the number of cardholders on your team or layering on manual approvals often slows the build and increases workarounds.

A more streamlined approach is implementing a modern card program with workflows that incentivize team compliance without adding friction.

As you review your current card program, ask where routine purchases feel harder than they should be, where field spend is most difficult to see in your reporting, and which card approvals depend on emails and spreadsheets.

These answers help you determine where a modern card program with streamlined controls can make spend management automated, efficient, and easy.