Why Your Construction Company Needs a Modern Credit Card Program

Why Your Construction Company Needs a Modern Credit Card Program

(Not just personal cards and reimbursements)

Many construction companies already run a credit card program. It just happens to live in the personal wallets of their team members.

When your superintendents, project managers, and executives put job costs on personal cards and submit expense reports later, it feels flexible. The team buys what they need, jobs keep moving, and accounting reconciles everything at month-end. On the surface, this type of system works.

The problem is not what you see right away. It is what stays hidden until it shows up as margin erosion, delayed reporting, or tension between the field and the office.

Where personal cards quietly break down

Personal cards shift financial responsibility away from the business and onto individuals. That tradeoff becomes increasingly costly as your operations grow.

First, there is no control at the moment spending occurs. Company policies cannot prevent off-policy purchases or overspending. Finance only learns what happened after the personal card statement arrives as an expense report, well after the point when the money is spent and the job has moved on.

Second, project costs arrive late and incomplete. Field teams think in materials, equipment, and urgency, not GL accounts and cost codes. Receipts come in batches, often with limited context about which job a charge belongs to. By the time expenses are properly coded, WIP reports and margin analysis are already outdated.

Third, receipt management turns into a monthly scramble. Documentation lives in trucks, personal inboxes, and phone camera rolls. Accounting spends valuable time tracking everything down, while audit and owner-reporting risk quietly increases.

Finally, personal cards create personal financial risk. When a superintendent puts thousands of dollars on a personal card to keep a job on schedule, they are effectively extending their own credit to the company and trusting that reimbursement timelines will hold.

In a small operation, these issues might be manageable. As job count, spend volume, and field headcount increase, they become systemic risk. This is often the point when teams start seeing unexplained margin fade and slower closes.

(Not just personal cards and reimbursements)

Many construction companies already run a credit card program. It just happens to live in the personal wallets of their team members.

When your superintendents, project managers, and executives put job costs on personal cards and submit expense reports later, it feels flexible. The team buys what they need, jobs keep moving, and accounting reconciles everything at month-end. On the surface, this type of system works.

The problem is not what you see right away. It is what stays hidden until it shows up as margin erosion, delayed reporting, or tension between the field and the office.

Where personal cards quietly break down

Personal cards shift financial responsibility away from the business and onto individuals. That tradeoff becomes increasingly costly as your operations grow.

First, there is no control at the moment spending occurs. Company policies cannot prevent off-policy purchases or overspending. Finance only learns what happened after the personal card statement arrives as an expense report, well after the point when the money is spent and the job has moved on.

Second, project costs arrive late and incomplete. Field teams think in materials, equipment, and urgency, not GL accounts and cost codes. Receipts come in batches, often with limited context about which job a charge belongs to. By the time expenses are properly coded, WIP reports and margin analysis are already outdated.

Third, receipt management turns into a monthly scramble. Documentation lives in trucks, personal inboxes, and phone camera rolls. Accounting spends valuable time tracking everything down, while audit and owner-reporting risk quietly increases.

Finally, personal cards create personal financial risk. When a superintendent puts thousands of dollars on a personal card to keep a job on schedule, they are effectively extending their own credit to the company and trusting that reimbursement timelines will hold.

In a small operation, these issues might be manageable. As job count, spend volume, and field headcount increase, they become systemic risk. This is often the point when teams start seeing unexplained margin fade and slower closes.

What a commercial credit card program changes

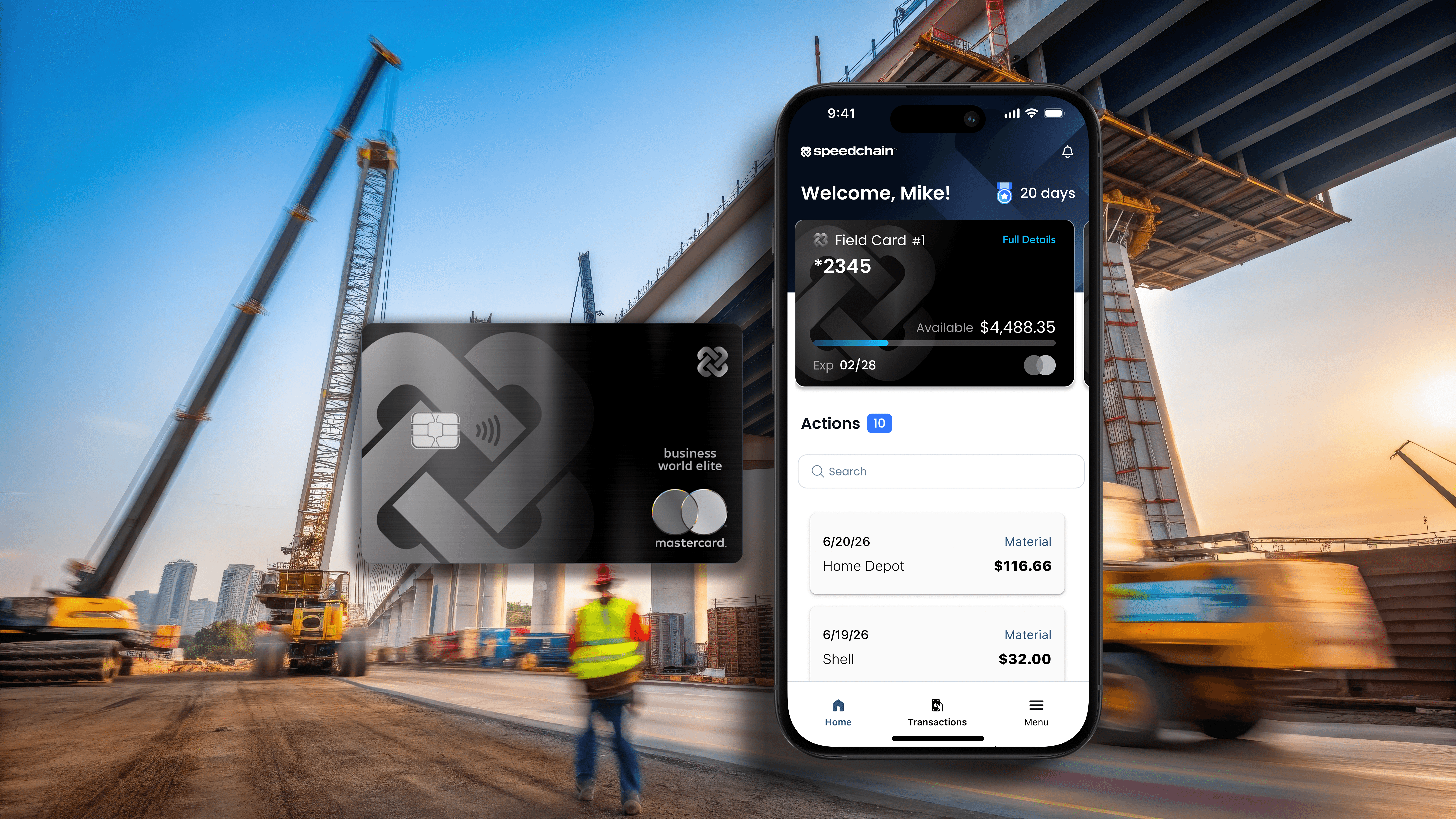

A modern commercial credit card program is not about issuing more cards that you have to manually track. Instead, these types of cards are designed so that controls, visibility, and accountability are built into workflows from the beginning.

Connected, company-issued credit cards ensure purchases are tied to the business, not personal credit. Clear limits and merchant rules define what different team members can spend before issues arise. Mobile receipt capture and job costing features eliminate guesswork later. Real-time visibility gives finance and leadership insight with sufficient time to act.

Most importantly, the process works the same way across field and the office operations. The spend process is structured correctly from the point of implementation, eliminating the need for “forensic accounting” after the fact.

Why this matters as your company scales

Moving away from personal cards streamlines daily operations and protects margin.

You see margin pressure earlier in a project, while there is still time to adjust behavior or rebalance spending. Field teams follow a straightforward expense management process that keeps pace with the jobsite. Accounting shifts from chasing receipts to analyzing results. Leaders gain confidence in equipping their team with cards, knowing they won’t lose visibility or control with scale.

Key differences and next steps

Personal cards and reimbursements lead to delayed spend visibility, inconsistent job coding, manual cleanup, and personal financial risk for your team members and your business.

In contrast, a modern commercial credit card program provides company-issued cards, built-in limits and controls, real-time job costing, and a consistent workflow that scales easily.

If you are evaluating your current credit card and spend management process, a good place to start is with these three questions:

1. Where do you lack financial visibility today?

2. Who is carrying personal financial risk on behalf of the company?

3. How early do you see project costs each month?

The answers usually make the next step clear.

What a commercial credit card program changes

A modern commercial credit card program is not about issuing more cards that you have to manually track. Instead, these types of cards are designed so that controls, visibility, and accountability are built into workflows from the beginning.

Connected, company-issued credit cards ensure purchases are tied to the business, not personal credit. Clear limits and merchant rules define what different team members can spend before issues arise. Mobile receipt capture and job costing features eliminate guesswork later. Real-time visibility gives finance and leadership insight with sufficient time to act.

Most importantly, the process works the same way across field and the office operations. The spend process is structured correctly from the point of implementation, eliminating the need for “forensic accounting” after the fact.

Why this matters as your company scales

Moving away from personal cards streamlines daily operations and protects margin.

You see margin pressure earlier in a project, while there is still time to adjust behavior or rebalance spending. Field teams follow a straightforward expense management process that keeps pace with the jobsite. Accounting shifts from chasing receipts to analyzing results. Leaders gain confidence in equipping their team with cards, knowing they won’t lose visibility or control with scale.

Key differences and next steps

Personal cards and reimbursements lead to delayed spend visibility, inconsistent job coding, manual cleanup, and personal financial risk for your team members and your business.

In contrast, a modern commercial credit card program provides company-issued cards, built-in limits and controls, real-time job costing, and a consistent workflow that scales easily.

If you are evaluating your current credit card and spend management process, a good place to start is with these three questions:

1. Where do you lack financial visibility today?

2. Who is carrying personal financial risk on behalf of the company?

3. How early do you see project costs each month?

The answers usually make the next step clear.